- Why IsraelThe story behind the success of Israeli innovation

- Ecosystem GrowthWe enhance the tech ecosystem and possess the expertise to utilize Israeli startups effectively in addressing current demands

- Global PartnershipsWe fortify the tech ecosystem by building bridges between local entrepreneurs and global partners

- AboutDiscover a wealth of resources tailored to support your journey in the vibrant Israeli startup ecosystem

- Content HubIsrael’s Impatient Innovation is shaping the future. Read and explore.

Tech Ecosystem

Tech Ecosystem Human Capital

Human Capital Focus Sector

Focus Sector The Health Network

The Health Network

Business Opportunities

Business Opportunities Investment in Israel

Investment in Israel Innovation Diplomacy

Innovation Diplomacy Leadership Circle

Leadership Circle

Discover

Filters

Format

Topics

All content

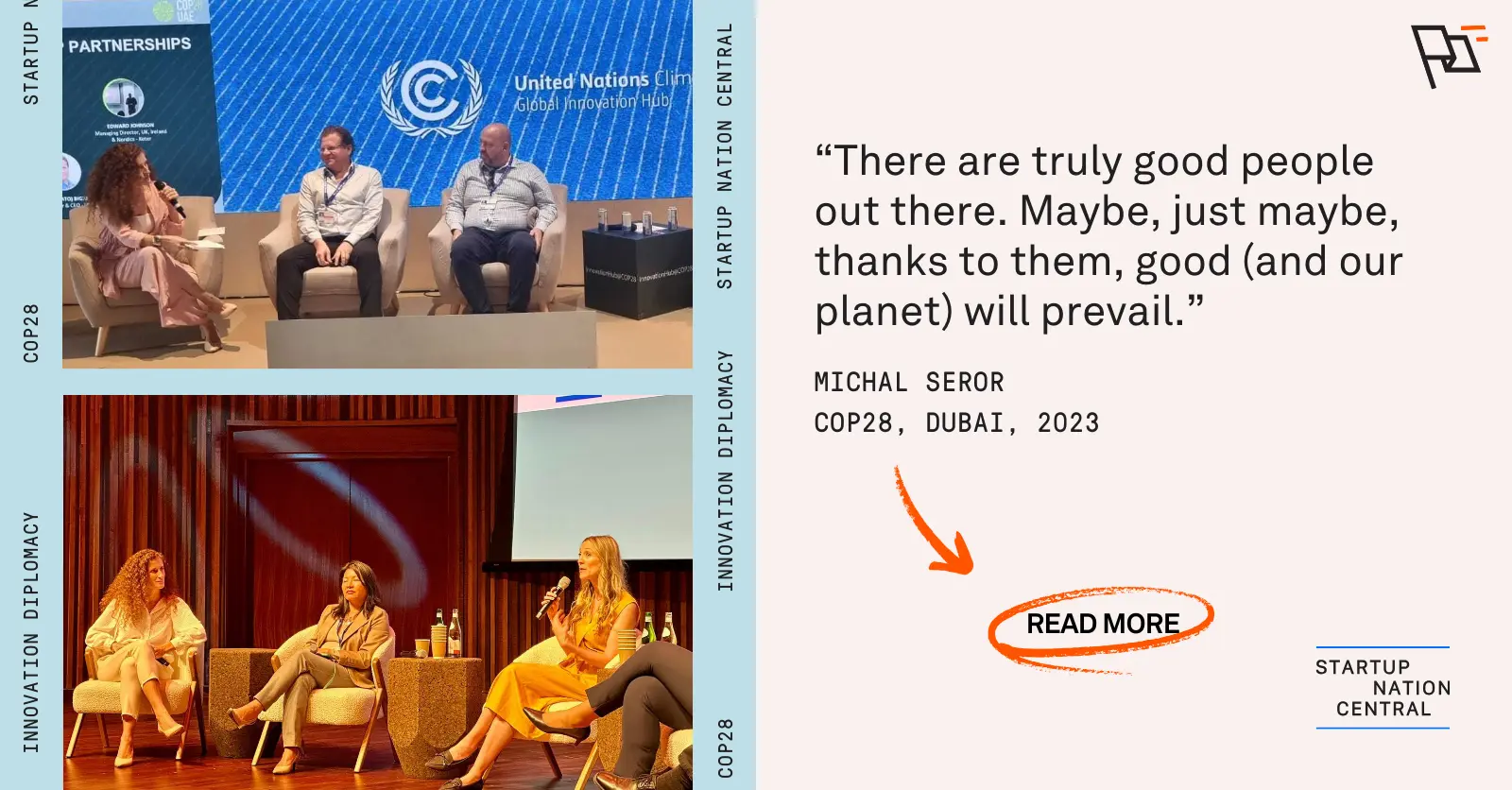

From Startup Nation to Startup Region: Cooperation Built Over Time

December 2025Innovation Diplomacy

NATO’s Innovation Shift and the Value of Israel’s Defense Mindset

December 2025Defense Tech

Abraham Accords: Tech Investments Redefining Cross-Border Collaboration

December 2025Innovation Diplomacy

How to Start a Business in Israel in 2026: A Guide for Entrepreneurs

December 2025Tech Innovation

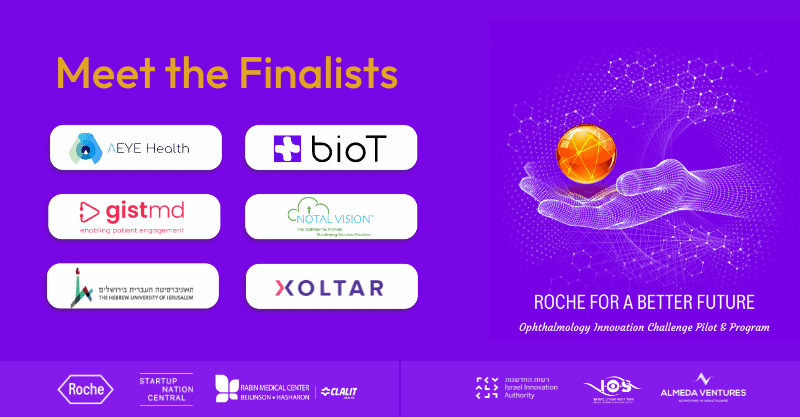

Roche for a Better Future Challenge: Advancing Digital Innovation for Women Living with Breast Cancer

December 2025Health Tech

Israeli Semiconductor Industry from Startup Nation to Global Powerhouse

December 2025semiconductor

Israel’s GDP Growth Drivers: High Tech, Innovation, and Beyond

November 2025Tech Innovation

PR: Israel’s “Two-Engine Paradox” Drives $40B in Chip Exits Since 1996 and $0.5B Annual Funding Amid Global Supply Shift

November 2025Tech Innovation

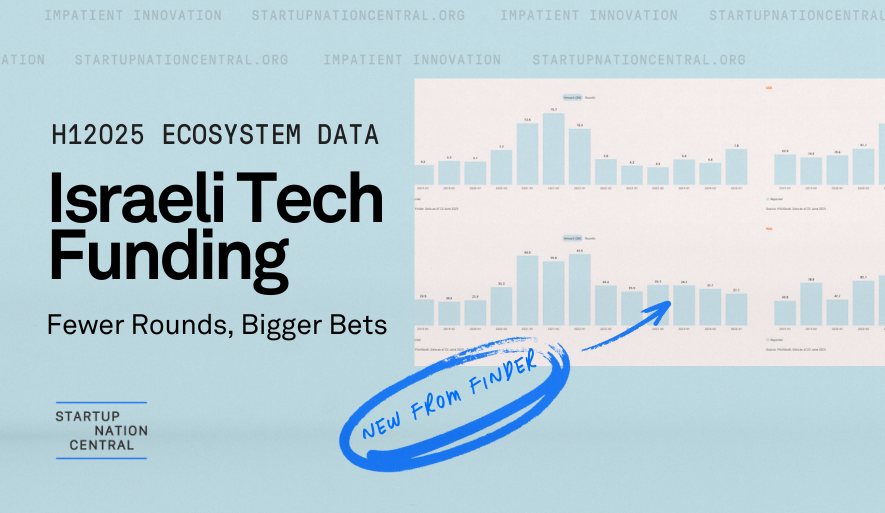

PR: Israeli Tech Sees Record-Breaking $71B in M&As in 2025 Despite Decline in Funding Rounds in Q3 2025

October 2025Finder

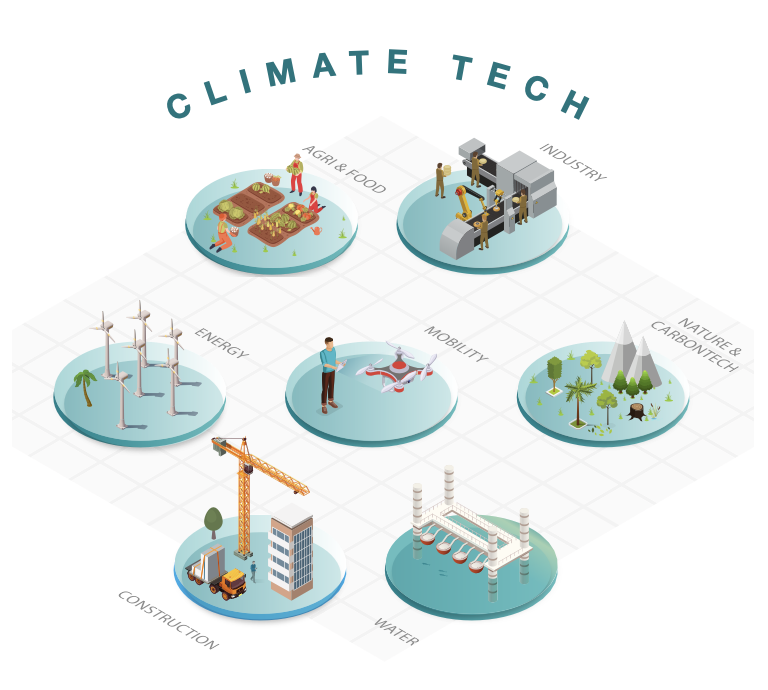

PR: Global Investors Head to Israel to Fund Breakthrough Climate Tech Startups

September 2025

The State of Innovation – Why and How Multinationals Innovate in Israel

September 2025Tech Innovation

Corporate Innovation is Driving Business Growth and Transformation

April 2025Tech Innovation

The Potential of AI Agents: Global Advances and Israel’s Unique Contributions

March 2025AI

Small Nations, Big Innovation: Lessons from Israel and Estonia

February 2025Innovation Diplomacy

Financing First-of-a-Kind Climate Projects: Downloadable Roadmap

November 2024Climate Tech

SynBio and Bio Convergence: Israeli Tech Transforming Global Innovation

November 2024Synthetic Biology

How Tel Hai and Startup Nation Central Are Shaping Israel’s Tech Talent

October 2024Human Capital

Advancing Israeli Leadership in the Future of Synthetic Biology

October 2024Human Capital

Top Ten Deals of the Year: Israeli Tech Startups, Game-Changing Investments

September 2024Investor

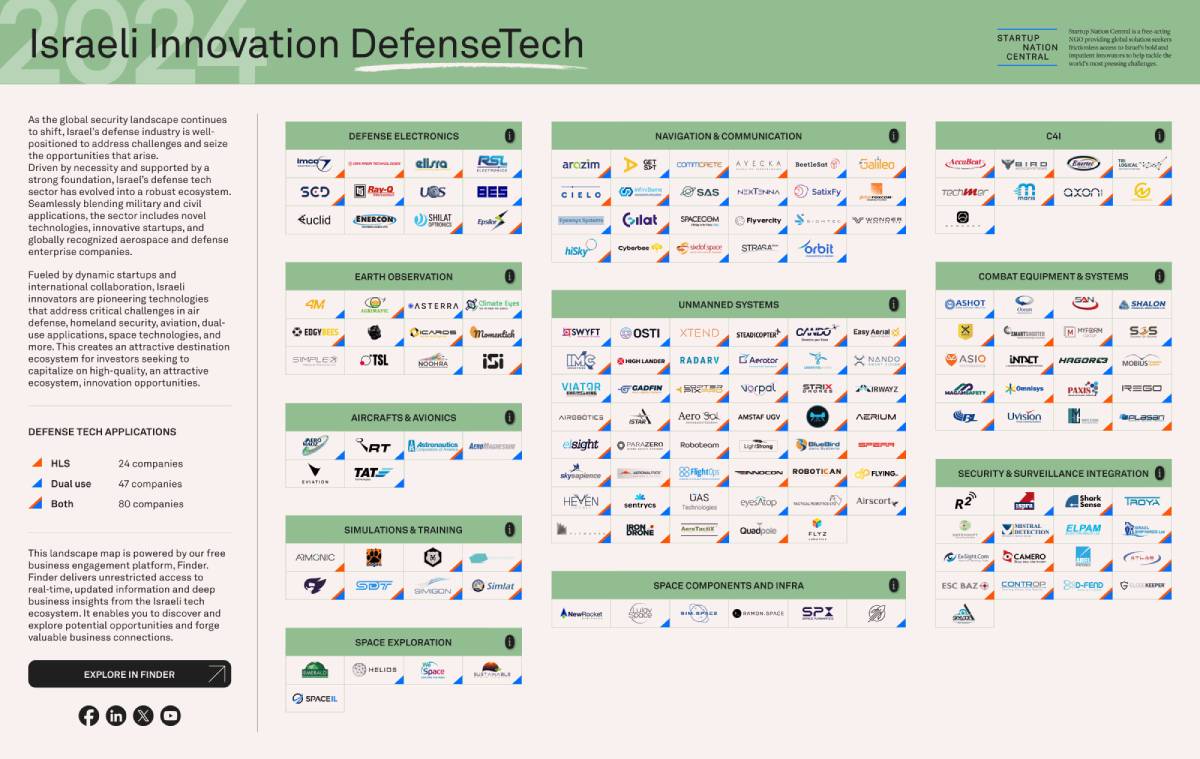

UGV and UAV Tech: Israel’s Unmanned Defense Systems Lead the Way

September 2024Defense Tech

Empowering Israeli Startups to Scale and Succeed: Startups First Initiative

August 2024Tech Innovation

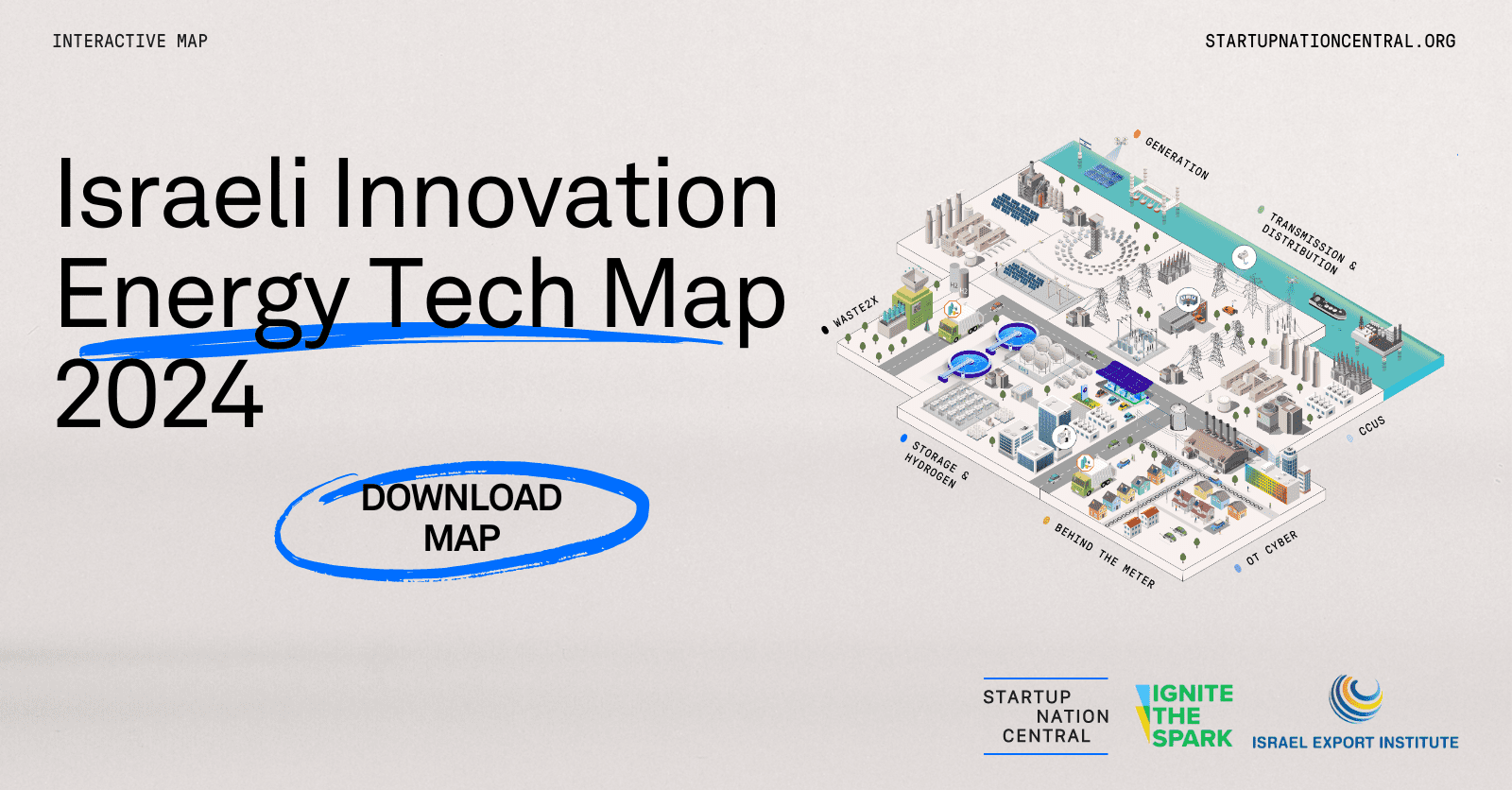

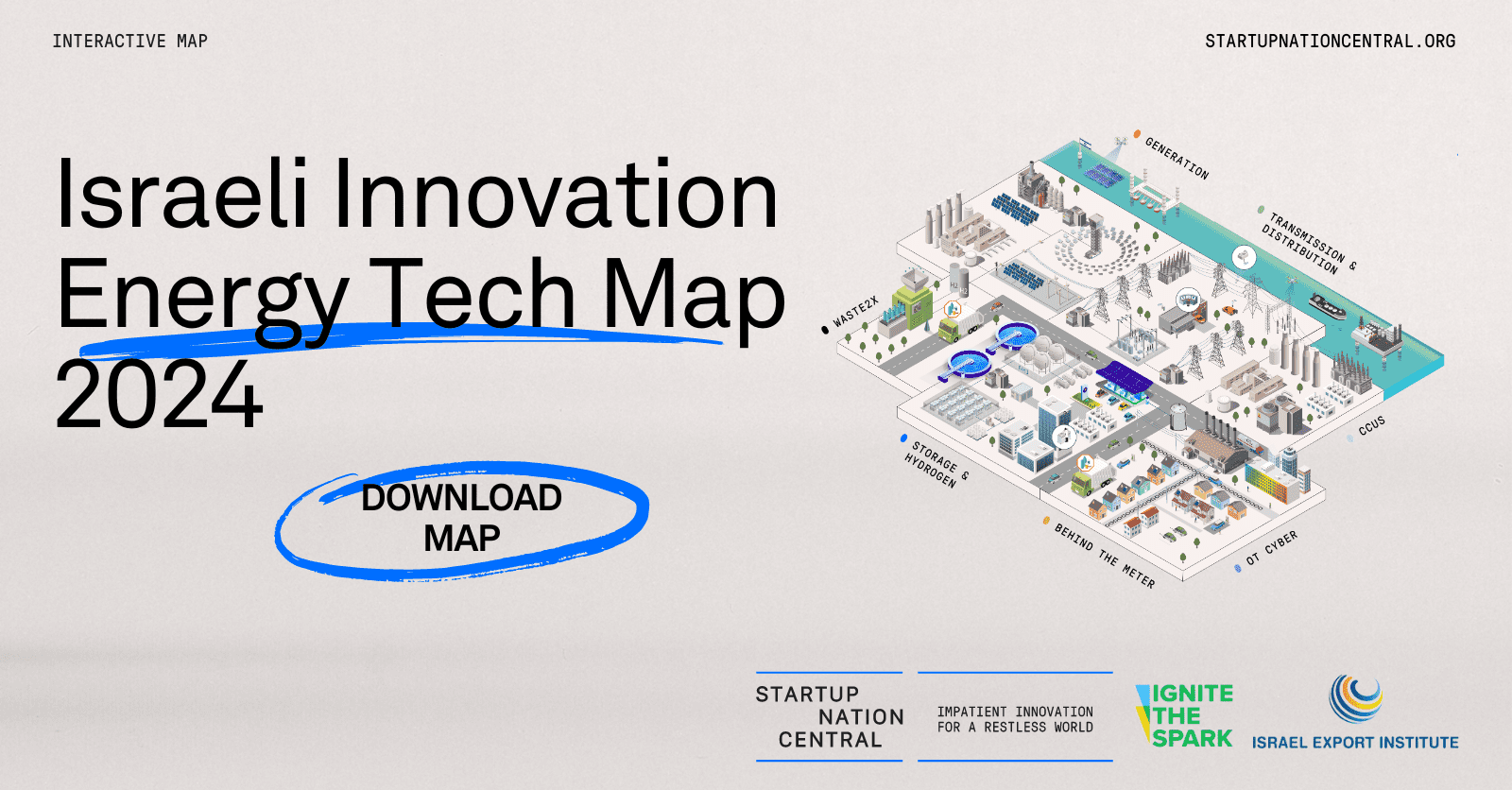

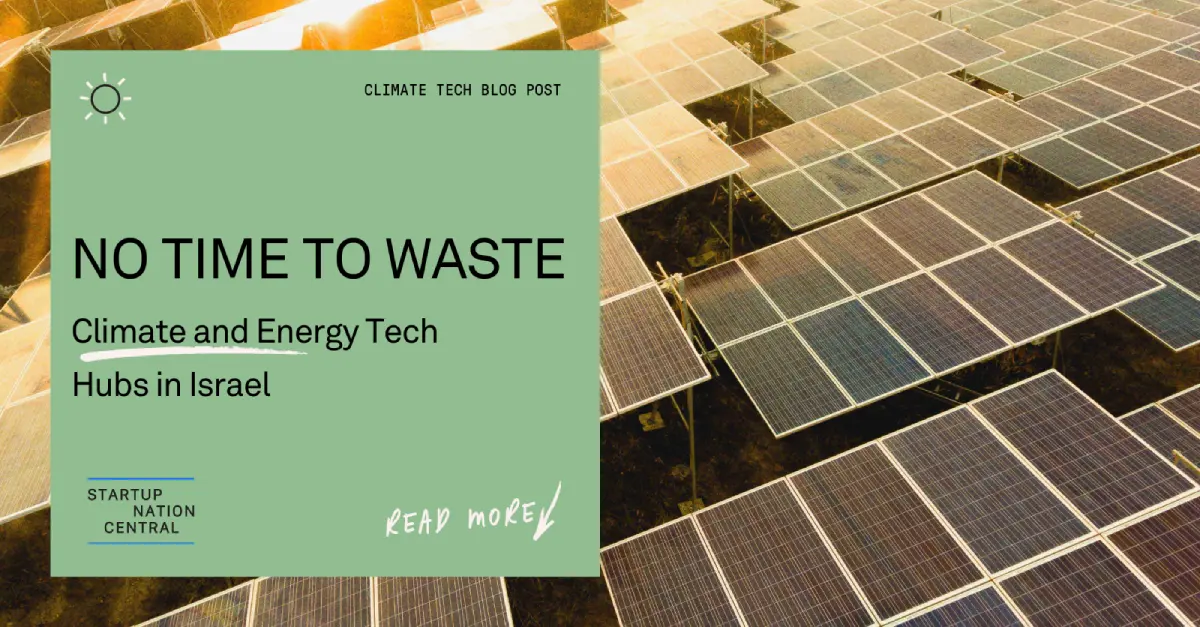

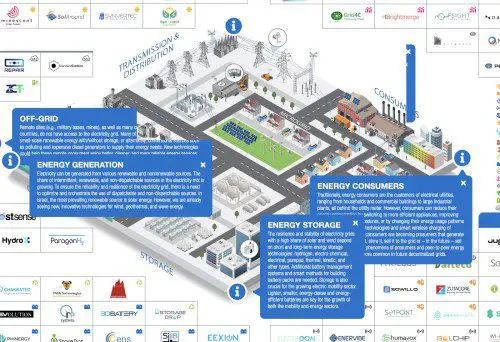

Powering the Future: The Role of Israeli Innovation in Advancing Energy Tech

July 2024Climate Tech

Israel’s innovation leadership spans its 76-year history — and beyond

May 2024Tech Innovation

Israeli Climate Innovation for Energy and Water Security Solutions

April 2024Climate Tech

Israeli Tech Q1 2024: Resilient Growth in a Challenging Landscape

April 2024Tech Innovation

The Essential Tools for Adapting Your Start-Up to the US Healthcare System

April 2024Health Tech

The Israel Biotech Revolution: AI, Collaboration, and Shaping the Future

March 2024Health Tech

Startup Nation Central Presents Israeli Tech Annual Report 2023

January 2024Tech Innovation

Tech Transfer and Scaling Health and Climate Innovation Solutions

December 2023Climate Tech

PR: Investments and M&A Activity Reach One Billion Respectively Since Oct. 7

November 2023Tech Innovation

Continued Deal Flow is an Indicator of Israeli Tech Investment Opportunity

November 2023Tech Innovation

Amid Conflict, Israel’s Tech Sector Embodies Resilience and Innovation

October 2023Tech Innovation

A New Era of Collaborative Prosperity for the Middle East

September 2023Innovation Diplomacy

Morocco’s Innovation Ecosystem: Breaking Silos, Building Collaboration

September 2023Innovation Diplomacy

Hospital2Hospital Clinical Capacity Tech Challenge: The Finalists

September 2023Health Tech

Innovation Diplomacy: Bringing Israel’s Startup Nation Story to the World

August 2023Innovation Diplomacy

H1 2023 Tech Reports: Navigating Uncertainty in Israel’s Innovation Ecosystem

August 2023Tech Innovation

Start-Up Nation Central’s Mid-2023 Reports Analyzes the Israeli Tech Sector

August 2023Tech Innovation

Off the beaten track: Israeli innovation is NOT confined to Tel Aviv

July 2023Tech Innovation

Dan Senor: UAE-Israel Tech Ties Like Tailor-Made Silicon Valley

July 2023Innovation Diplomacy

SNC Honored for Contributions to Morocco’s FRDISI Foundation

July 2023Innovation Diplomacy

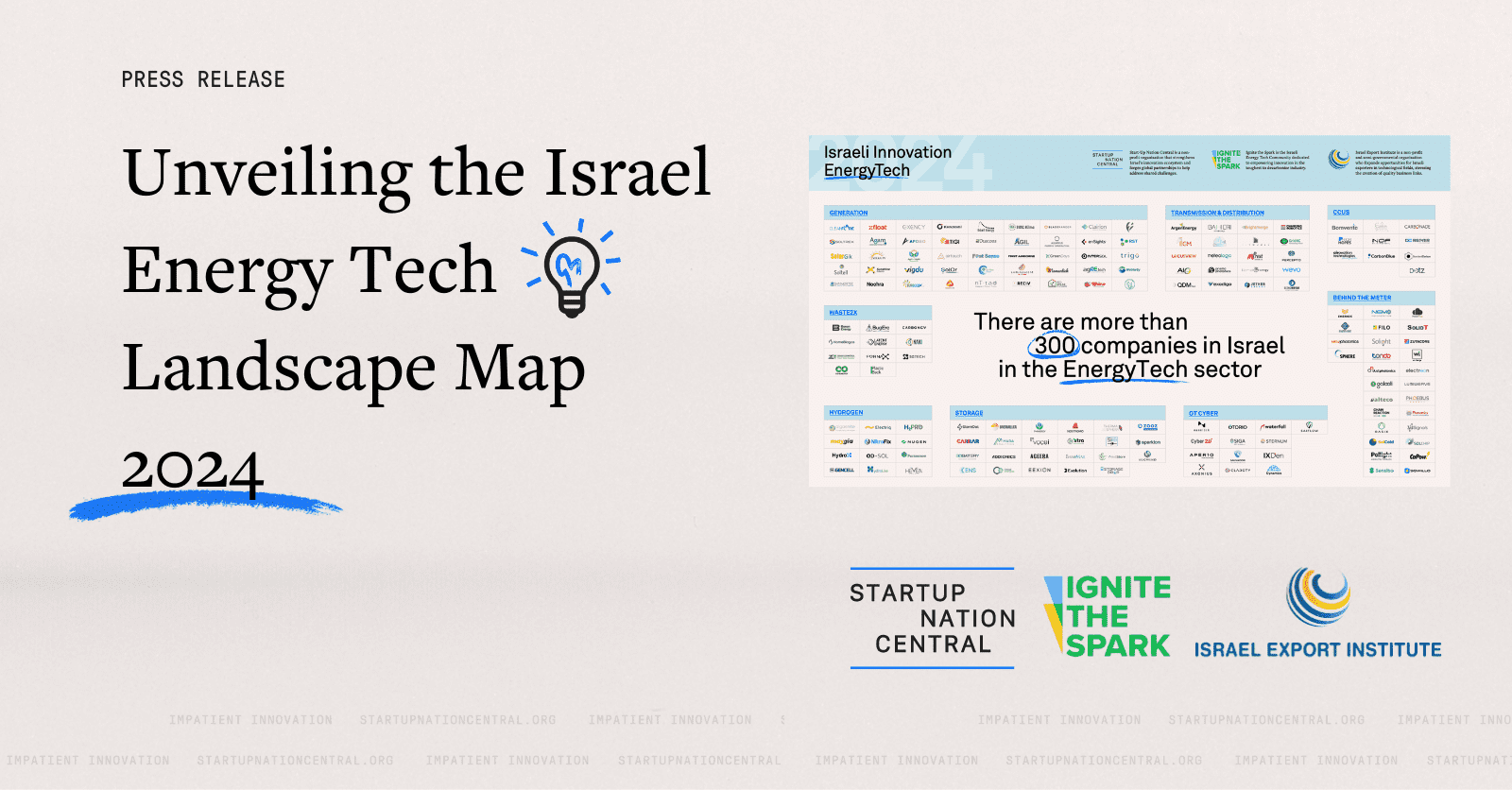

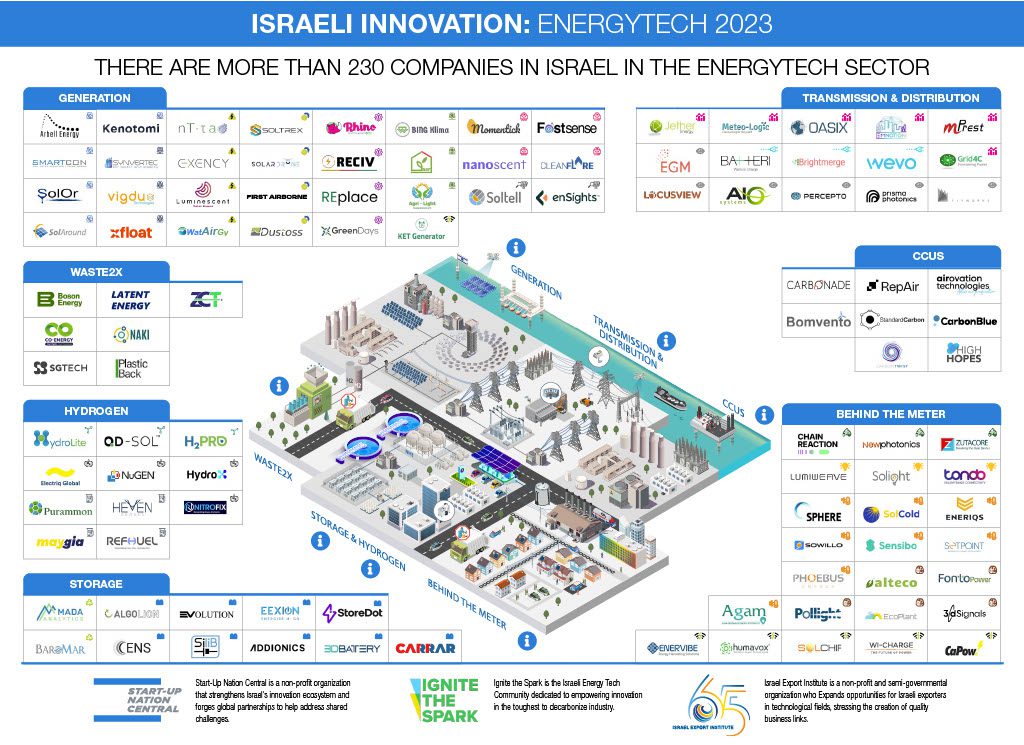

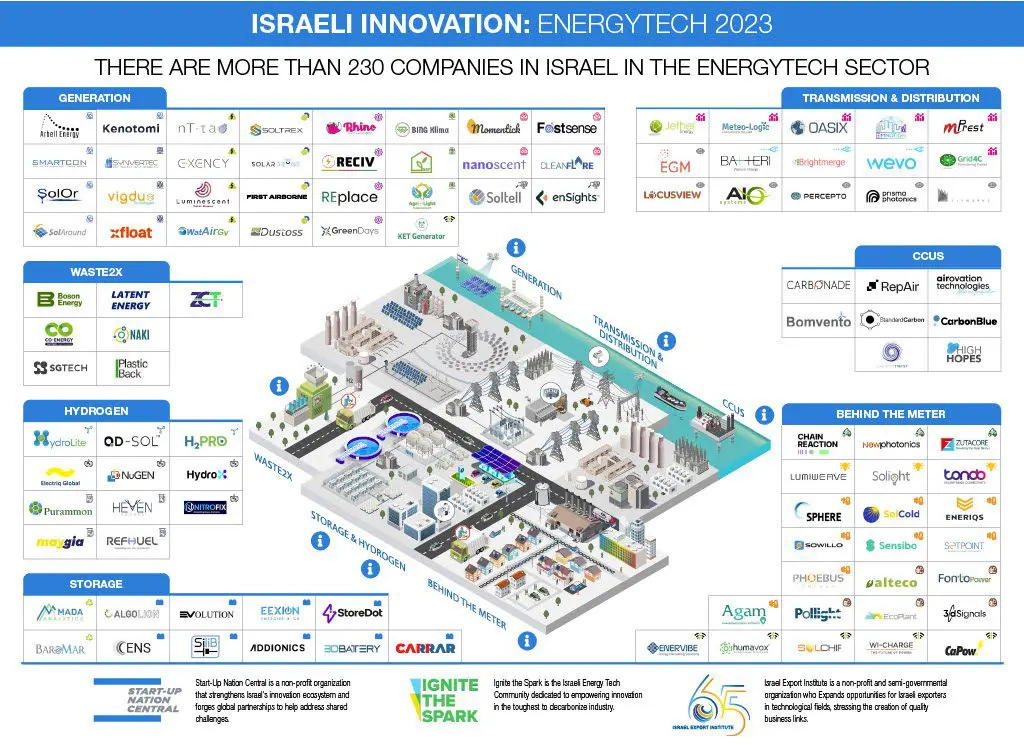

Number of Israeli EnergyTech Companies grow to more than 230 in 2023

June 2023Climate Tech

Global Women Leaders Unite to Shape the Future of Innovation

May 2023Innovation Diplomacy

The Israeli Cybersecurity Tech Sector Q1 2023 Report by Start-Up Nation Central

May 2023Cyber Security

The Israeli Enterprise IT & Data Sector Q1 2023 Report by Start-Up Nation Central

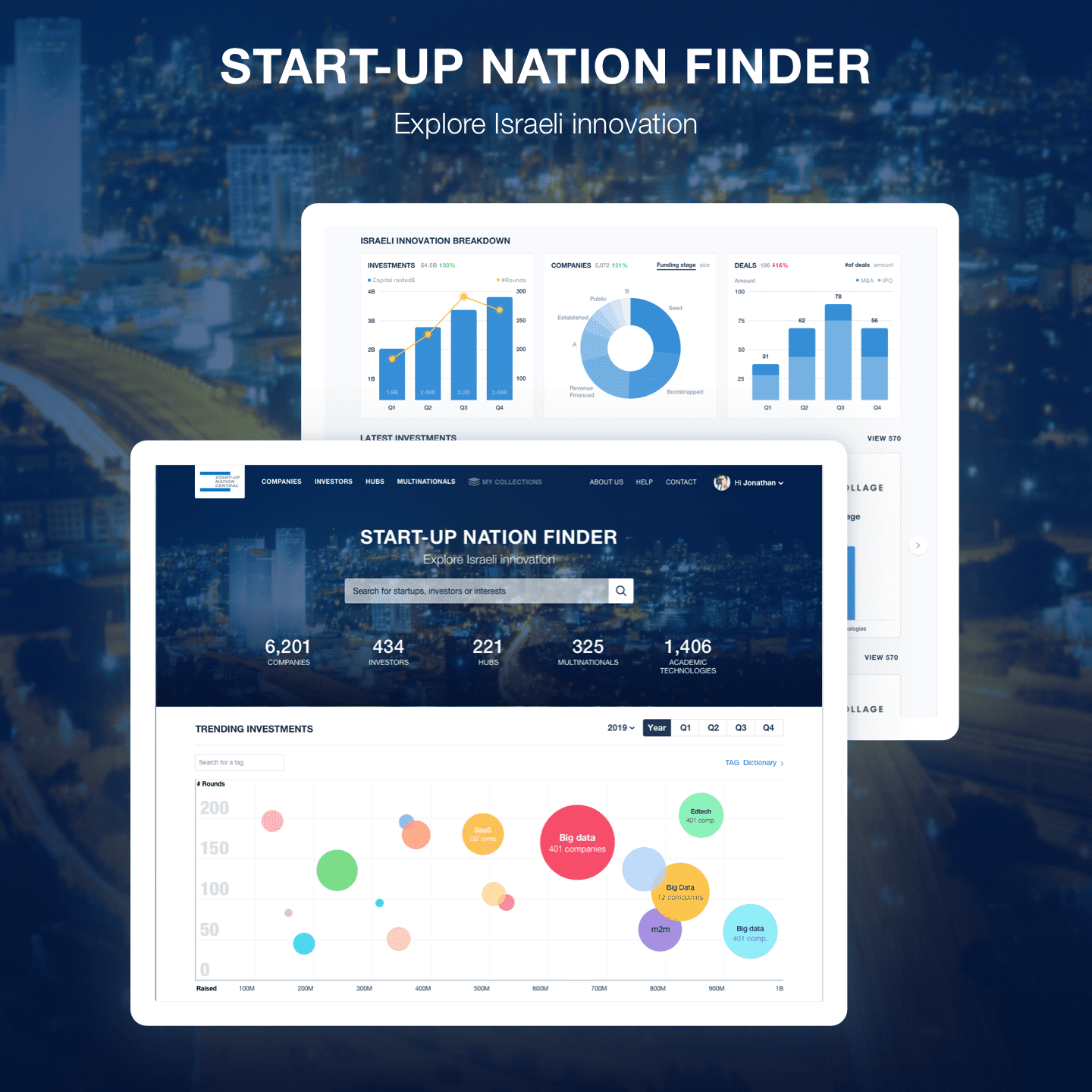

May 2023Finder

The Israeli Agriculture & Food Tech Sector Q1 2023 Report by Startup Nation Central

May 2023Finder

The Israeli Health Tech Sector Q1 2023 report by Start-Up Nation Central

May 2023Finder

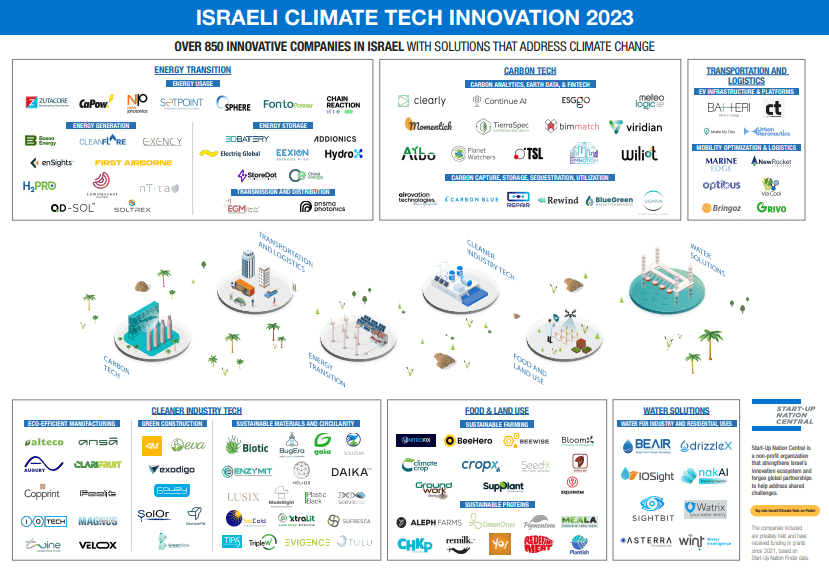

The Israeli Climate Tech Sector Q1 2023 Report by Start-Up Nation Central

May 2023Climate Tech

A Hidden Gem Emerges: Israel is a Focus in the Digital Health Industry

April 2023Health Tech

Innovation Without Borders: Israel and Bahrain Partner for Progress

March 2023Innovation Diplomacy

Israel and Bahrain Are Taking Their Relationship to a New Phase

March 2023Innovation Diplomacy

The “Connect2Innovate” conference to kick off in Bahrain in March

March 2023Innovation Diplomacy

The “Connect2Innovate” conference to kick off in Bahrain in March

February 2023Innovation Diplomacy

Moroccan Delegation Visits Israel to Expand Tech Collaboration

January 2023Innovation Diplomacy

Israel needs to seize climate tech market opportunity – opinion

December 2022Climate Tech

EyeKnow Wins Henry Ford Health & Start-Up Nation Central Challenge

December 2022Health Tech

Start-Up Nation & UM6P Promote Innovation Knowhow Partnership

November 2022Innovation Diplomacy

Start-Up Nation Central & UM6P Partner to Advance Innovation

November 2022Innovation Diplomacy

Israel can help the Middle East in the battle against climate change

November 2022Climate Tech

More than $2 million awarded to Israeli Climate Tech researchers and startups

October 2022Climate Tech

How we’re reducing the carbon footprint of the Climate Solutions Festival

October 2022Climate Tech

Solving Land and Light Challenges: Meet Ilan Sharon of Red Solar

September 2022Climate Tech

Two years of the Abraham Accords: Tech and innovation play a critical role

September 2022Innovation Diplomacy

The future is bright for Israel-Bahrain business, economy ties – opinion

September 2022Innovation Diplomacy

Abu Dhabi Global Market and Start-Up Nation Central Partner

September 2022Innovation Diplomacy

The Corporate Innovation Partner Connecting Israeli Tech Globally

August 2022Tech Innovation

From defense intelligence to tree intelligence, meet Israel Talpaz of SeeTree

August 2022Agritech

Meet the AgriTech investor building a better world for future generations.

July 2022Agritech

Overcoming obstacles to implementing innovation through successful POCs

June 2022Tech Innovation

Innovation can cement Israel and Morocco’s budding relationship

May 2022Innovation Diplomacy

A decline in the number of new startups: Cause for concern or natural maturation?

May 2022Tech Innovation

“We are the engine behind Finder.” Q&A with info specialist Maor Perlov.

April 2022Tech Innovation

Let’s not miss the opportunity to make Israel a ClimateTech leader

April 2022Climate Tech

Report: Drop in Ad and Social Media Startups Hurts Israel’s Tech

April 2022Tech Innovation

Iran is not the only threat that Middle East countries can unite around

April 2022Innovation Diplomacy

Israeli institutional investors bursting onto the local VC scene

March 2022Tech Innovation

ISRAELI AGRIFOOD-TECH & WATER-TECH SECTORS CONCLUDE RECORD-BREAKING YEAR

March 2022Agritech

What’s the key to adapting Industry 4.0 innovation? Simplicity.

March 2022Tech Innovation

Start-Up Nation Central and FemTech Israel map the local FemTech Landscape

March 2022Health Tech

Worried about the quality of your water? Don’t just purify, nutrify.

February 2022Food Tech

Sky-Mining: Airovation Technologies converts CO2 into valuable minerals

February 2022Climate Tech

Israel’s reclassification by MSCI is a boon to the country and tech investors

January 2022Tech Innovation

Roland Berger & Start-Up Nation Central Partner on GCC Innovation

January 2022Innovation Diplomacy

UN Ambassadors Visit Israel Hosted by Start-Up Nation Central

December 2021Innovation Diplomacy

UN Ambassadors Visit Israel to Learn About Sustainability Tech

December 2021Innovation Diplomacy

The UAE Embassy in Israel partners with Start-Up Nation Central…

November 2021Innovation Diplomacy

ISRAELI DIGITAL HEALTH STARTUPS ADDRESSING GLOBAL PHARMA CHALLENGES 2021

November 2021Health Tech

Colombian President Visits SNC to Explore Israeli Innovation

November 2021Innovation Diplomacy

UAE Education Minister Explores Israeli EdTech Solutions

November 2021Innovation Diplomacy

How Does Israel’s Innovation Ecosystem Compare to 9 Global Tech Hubs?

November 2021Tech Innovation

Finding Big Impact Investment Opportunities in One Small Country

October 2021Climate Tech

Who is Responsible for the Large Increase in Investment in Israeli High-Tech?

August 2021Finder

Start-Up Nation Central awarded Yigal Allon Prize for Pioneering Excellence

July 2021Tech Innovation

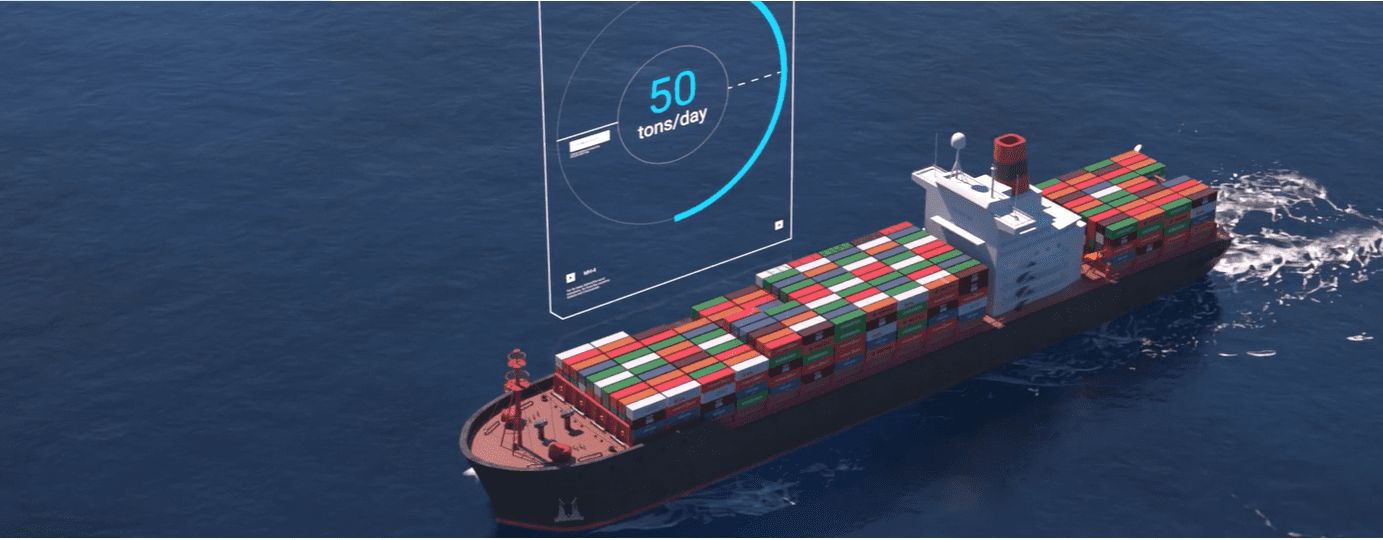

Israeli Smart Logistics Innovators Strengthen Global Supply Chains

May 2021Tech Innovation

UAE and Israel Launch Joint Task Force for Tech Innovation

April 2021Innovation Diplomacy

Israel-India bilateral accelerator lands major deals for Israeli start-ups

April 2021Innovation Diplomacy

What Does the Increase in Closures of Israeli Start-ups Really Mean?

March 2021Tech Innovation

The world can learn more than meets the eye from Israel’s vaccine program

February 2021Health Tech

Meet the Finalists: Israeli Startups that Provide Innovative Solutions to Global Environmental Challenges to Present at ‘SustainIL’

January 2021Climate Tech

SNC launches UAE-IL Tech Zone, the first UAE-Israel innovation community

December 2020Innovation Diplomacy

UAE Minister: Strong Need for UAE–Israel AI Collaboration

December 2020Innovation Diplomacy

Beyond Automotive: Why Michigan is Eying Israeli Industry 4.0 Innovation

November 2020Tech Innovation

Join the Industry 4.0 Global Summit on Post-COVID Digitization

November 2020Tech Innovation

The Impact Revolution: From Sustainable Development Goals to Tech Solutions

November 2020Climate Tech

COVID-19 Sparks a New Social Contract in Israel’s Tech Sector

October 2020Tech Innovation

Israel, India sign MoU to collaborate on tech innovation

September 2020Innovation Diplomacy

Will Urban Hubs Remain Centers of Innovation Post-Pandemic?

September 2020Tech Innovation

Virgin Atlantic CIO: “Israel is one of the most innovative places on the planet”

September 2020Tech Innovation

Why Israeli Startups Should Choose Houston as Their U.S. Gateway

August 2020Tech Innovation

Start-Up Nation Central, IDB Boost Israel–Latin America Tech Ties

August 2020Innovation Diplomacy

COVID-19 Presents a Digital Transformation Opportunity for Manufacturers

August 2020Tech Innovation

Sweden and Israel Partner to Drive Innovative R&D Projects

August 2020Innovation Diplomacy

Will Israeli FinTech Continue to Thrive in the Post-Coronavirus Era?

July 2020Tech Innovation

Developments in FDA, HIPAA and IP Processes in light of the Emergency status

May 2020Tech Innovation

Balancing Public Health And Data Privacy: Where Does COVID-19 Meet Cybersecurity?

May 2020Cyber Security

80 Israeli MedTech Companies Take On The Global Fight Against Coronavirus

April 2020Health Tech

Five Ways to Tackle the Human Capital Shortage in Israel’s High-Tech Industry

February 2020Human Capital

Impact Nation: Israeli Innovations Taking On The UN’s Sustainable Development Goals

February 2020Climate Tech

Global Industrial Giants Set To Attend Israel Industry 4.0 Innovation Week

February 2020Tech Innovation

For Industry 4.0 To Take Off, It Needs Industries 2.0 & 3.0 To Join The Party

February 2020Tech Innovation

Space Week 2020: Meet the Startups Propelling Israel’s SpaceTech Industry

January 2020Tech Innovation

Joining the Unicorn Club: Israel’s AppsFlyer Raises $210M at $1.6 Billion Valuation

January 2020Tech Innovation

Texas Governor Urges Deeper Collaboration With Innovative Israeli Tech

January 2020Tech Innovation

Israeli Startups Revolutionize Industry 4.0 with Efficiency Tech

January 2020Tech Innovation

Insight Acquires Israeli Cybersecurity Startup Armis at $1.1B Valuation

January 2020Cyber Security

Joining The Billion-Dollar Club: Meet The Israeli ‘Unicorns’ Born In 2019

December 2019Tech Innovation

Israel’s Largest Financing Rounds Of 2019 Reveal Surge In Late-Stage Funding

December 2019Tech Innovation

Israel’s first team in Tour de France will promote the Startup Nation

December 2019Tech Innovation

Nine Israeli Technologies Among TIME Magazine’s 100 Best Inventions

December 2019Tech Innovation

Israeli Logistics Startup ‘Fabric’ Raises $110 Million to Expand its US Operations

October 2019Tech Innovation

Digital Therapeutics – Pushing Israeli Digital Health Forward into the Future

April 2019Health Tech

Our New Paradigm for Energy Efficiency and Maintenance in Manufacturing

December 2018Climate Tech

Blockchain Regulation Now and Into the Future – What We Can Expect

December 2018Tech Innovation

A Guide To The Latest Hacker’s Business Model And How To Beat it

November 2018Cyber Security

$32m Raised by Velox, Direct-to-Shape Digital Printing Company

November 2018Tech Innovation

Grid4C, Smart Grid Predictive Analytics Startup, Raises $5 Million

November 2018Tech Innovation

CreditPlace Peer-to-Peer Debt Trading Startup Raises $8 Million

November 2018Tech Innovation

$30 Million Raised by Airobotics, Creators of Autonomous Drone Solutions

November 2018Tech Innovation

Israel Early-Stage VC “The Time” Invests 2.5M NIS in Maverick Medical AI Ltd

November 2018AI

$8M raised in seed funding by Vayavision, Tel Aviv-based providers of raw data fusion and perception systems for self-driving vehicles

October 2018Tech Innovation

Automated Skyscraper Window Cleaning Solution Providers Skyline Raise $3M

October 2018Tech Innovation

Start-Up Nation Central Wows Africa with Israeli Innovation

September 2018Tech Innovation

$14M in Series B Funding Raised by Israel-based AI Fintech Company Pagaya

September 2018AI

$3.1M Raised from French insurer AXA by Air Doctor, the Online Medical Marketplace for Tourists

August 2018Health Tech

3 Israeli Foodtech Start-Ups Chosen for Prestigious PepsiCo Nutrition Greenhouse Incubator Program

August 2018

Online Lender BlueVine Announces $12M Investment from Microsoft’s Venture Fund M12

August 2018

Start-Up Nation Central Aims to Help African Farmers by Teaming Up With African NGO

August 2018

European Sugar Producer Südzucker Partners with DouxMatok to Further Develop Innovative Sugar Reduction Technology

August 2018

$28M Raised in Series A Funding by Developers of AI and Computer Vision Technology AnyVision

July 2018

$21 M in Series A Funding Raised by Viz.ai for Solution to Increase Patient Access to Proven Therapies

July 2018

3 Israeli Start-ups on Shortlist for PepsiCo Nutrition Greenhouse Incubator Program

July 2018

ViAqua, Medical Aquafarming Startup Receives Investment from Nutreco – Dutch Animal Feed Company

July 2018

$10 Million Capital Raise to Drive Arbe Robotics’ Next-generation Autonomous Vehicle Sensing Technology

July 2018

$7 Million in Seed Funding Announced for Trigo’s Advanced Retail Automation Platform

July 2018

Announcing $15M Series B Led By Draper Nexus, SafeBreach Expands Leadership in Breach and Attack Simulation

May 2018

Cynerio Israel Ltd contracted to Protect MRI, Insulin Pumps from Cyber Attacks at Tel Aviv Sourasky Medical Center & Rambam Healthcare Campus

May 2018

$3.5 Million Raised in Series A Round by Fintech-Specialist Company Reach

April 2018Investor

Israeli Biotech Algatech Buys Stake in NZ-Based Microalgae Cultivation Company

April 2018

ActivePath Acquired by BroadRidge, Expected to Improve Communication Experiences through Interactivity

April 2018

Biocatch secures $30M in funding to redefine digital identity and renew trust in online interactions

March 2018

The Israeli Video Games Ecosystem: Converging Technologies, Emerging Opportunities

February 2018Investor

$20M in funding for CommonSense Robotics online grocery fulfillment robotics technology

February 2018

Multi-investor funding round for VDOO, creators of first-of-its-kind IoT security platform Picture suggestions

January 2018

From Start Up to Break-Through – a Comprehensive Toolbox for Digital Health Start Ups

December 2017Health Tech

Haier Israel Taps Start-Up Nation Central To Boost Innovation

October 2017Tech Innovation

Everything You Could Ever Want to Know about the Israeli Innovation Ecosystem

September 2017Finder

Follow the Money: Investors Seeing Israel in a New Cybersecurity Light

April 2017Cyber Security

Why does 15% of the World’s Investment in Cybersecurity go to Israel

February 2017Cyber Security

Why International Companies Are Investing in Israeli FinTech Start Ups

January 2017Investor

The New Players in the Game: How Start-ups are Changing Digital Health

December 2016Health Tech

DocAuthority, creators of AI-based data identification platform raises $10 million

January 1970

Caesarea-based Israeli cardiac imaging co EPD bought by Netherlands’ Royal Philips for $292m

January 1970

$17 million raised by IntSights to tackle growing cyber-risks for enterprises

January 1970

$3 million seed financing round closed by TriEye Ltd., developers of short-wave infrared (SWIR) imaging technology

January 1970

A Series A Round Led by HAHN Group, Raises $10M for Kitov Systems, AI-Based Automated Visual Inspection Pioneers

January 1970