- Why IsraelThe story behind the success of Israeli innovation

- Ecosystem GrowthWe enhance the tech ecosystem and possess the expertise to utilize Israeli startups effectively in addressing current demands

- Global PartnershipsWe fortify the tech ecosystem by building bridges between local entrepreneurs and global partners

- AboutDiscover a wealth of resources tailored to support your journey in the vibrant Israeli startup ecosystem

- Content HubIsrael’s Impatient Innovation is shaping the future. Read and explore.

Tech Ecosystem

Tech Ecosystem Human Capital

Human Capital Focus Sector

Focus Sector The Health Network

The Health Network

Business Opportunities

Business Opportunities Investment in Israel

Investment in Israel Innovation Diplomacy

Innovation Diplomacy Leadership Circle

Leadership Circle

Investment Opportunities in Israeli Tech

Capitalize on Israel's resilient tech ecosystem. With high-quality companies, low valuations, and groundbreaking solutions, now is the prime time to invest in a market driving global innovation.

Join Us

The time to invest in Israel is now

Israel's dynamic environment and the resilience of its tech startups create an attractive investment opportunity. Decades of national challenges have spurred innovation and improved efficiency, leading to new technologies and ensuring that Israeli tech delivers – no matter what.

Why Israel? Tech in Numbers

A powerhouse with a thriving innovation ecosystem

-

#1

Number of Startups

Per Capita

-

#4

R&D Investment

As % of GDP

-

#2

Innovation Linkages

-

#1

In Public Companies

Listed on Nasdaq

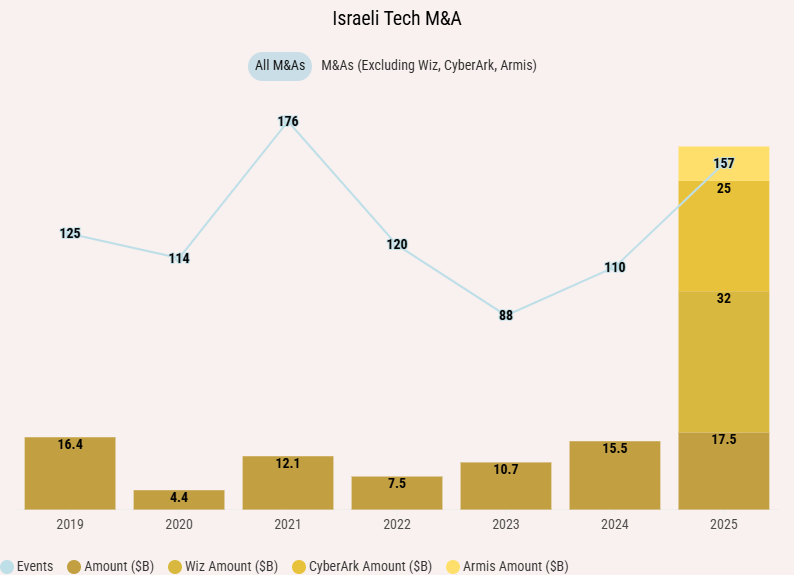

2025 M&A hits record high

Global buyers returned to Israel in force in 2025, driving M&A to record levels with $82.3B in disclosed value.

Learn More

MNC Innovation and R&D Centers

Israel is home to nearly 450 MNC Innovation and R&D Centers, indicating continued trust in its tech ecosystem, even with a slight decline this year. While challenges persist, the numbers remain strong. Dive into Finder to explore the key players driving innovation.

Explore the Ecosystem

Investing in Israeli Tech

For investors seeking high-growth, innovation-driven opportunities, now is the time to act. With over 7,000 startups and tech companies, 517 venture capital funds, and nearly 450 MNCs with innovation activity in Israel, the ecosystem is as dynamic and resilient as ever.

As your partner on the ground, Startup Nation Central is available to help new investors to Israel navigate and access these opportunities.

Read the Blog

As your partner on the ground, Startup Nation Central is available to help new investors to Israel navigate and access these opportunities.

Roadmap for Japanese Investors

From structured pilot projects to thriving cross-border partnerships, Japanese corporations such as Sony, Toshiba, and Mitsubishi UFJ have successfully collaborated with Israeli innovators to gain a competitive edge. This roadmap is your guide to navigating Israel’s thriving tech ecosystem, offering practical insights and strategies for integrating Israeli innovation into your growth journey.

Download Now

Roadmap for FOAK Climate Investing

A practical roadmap for FOAK financing, supported by real-world case studies of successful transactions, innovative financial structures, and key lessons from the field. Our insights aim to inspire pilot programs that connect technology, investors, and concessional capital to create scalable, impactful solutions.

Download Roadmap

Engage with Ease

Finder, the business engagement platform of the Israeli tech ecosystem

Get curated deal flow and dive into data, insights, and venture capital models that fit your portfolio’s needs.

Finder gives investors the ability to connect directly with Israeli innovators and explore strategic opportunities

Finder gives investors the ability to connect directly with Israeli innovators and explore strategic opportunities

We Are by Your Side

Seize smart investment opportunities with the right partner

At Startup Nation Central, we provide the support, data, and connections you need to thrive. Whether you're an investor, innovator, or global corporation, our platform facilitates strategic partnerships, investments, and growth opportunities. From joint ventures to R&D centers, we help you navigate Israel’s tech ecosystem, empowering your success.

Data and insights

Gain comprehensive market intelligence and trends for informed decision-making.

Curated deal flow

Access a stream of high-potential investment opportunities tailored to your interests.

Access to industry experts

Connect with leading experts for valuable guidance and market insights.

Venture capital models

Explore proven investment frameworks to maximize returns.

MNC innovation strategy

Develop customized strategies that align with the innovation goals of multinational corporations..

Impatient innovation

as a catalyst

for growth

Israeli innovators are driven by a sense of urgency to deliver quick and impactful solutions. This makes Israeli tech companies an ideal match for investors looking for fast, tangible results. Our impatient innovators aren't afraid to take risks, challenge formalities, and pivot swiftly in the face of obstacles, ensuring rapid progress and breakthroughs.

For investors eager to see their funds translate into meaningful growth quickly, Israel's bold and determined approach to innovation offers an unmatched opportunity to achieve those goals.

Learn more For investors eager to see their funds translate into meaningful growth quickly, Israel's bold and determined approach to innovation offers an unmatched opportunity to achieve those goals.

Case Studies

Scaling the impact of innovation through collaboration

Investor Roadshow: London, Zurich, Geneva

This investor roadshow highlighted Israeli innovation in climate and deep tech. The series gathered top Israeli venture capital funds, including Zora Ventures, Mobilion Ventures, Crescendo, Lumir Growth Partners, Disruptive AI Venture Capital, and Doral Energy-Tech Ventures.

Curated in partnership with the Economic and Trade Mission, the Embassy of Israel in London, Crescendo Partners, and Alma Angels, we created a space for dialogue and dealmaking between Israeli investors and European partners eager to invest in transformative technologies.

Curated in partnership with the Economic and Trade Mission, the Embassy of Israel in London, Crescendo Partners, and Alma Angels, we created a space for dialogue and dealmaking between Israeli investors and European partners eager to invest in transformative technologies.

German Automotive Roadshow: Driving Future Innovation

We led a delegation of Israeli startups to Germany, in partnership with the Israel Trade Office in Munich. The delegation showcased innovations in AI, predictive maintenance, machine learning, and big data to leading OEMs and tier 1 suppliers in the German automotive sector. This initiative fostered new partnerships and laid the foundation for future collaboration and growth between Israeli tech and Germany’s automotive industry.

2024 Luxembourg Roadshow: Automotive Innovation

A strategic delegation to Luxembourg, in collaboration with Luxinnovation, Technoport, and the House of Entrepreneurship, featured Ecomotion and several startups, fostering connections in the automotive industry. Key meetings with investors and automotive players explored funding opportunities and incentives. This collaboration laid the groundwork for new partnerships, strengthening ties between Israel and Luxembourg's automotive ecosystems.

Climate Week NYC 2024: Powering the Future of Climate Tech

At our exclusive, invite-only event during Climate Week NYC 2024, in partnership with NetZero Tech Ventures, we gathered over 100 investors and entrepreneurs to discuss the future of climate and energy solutions. Israeli tech stood out, with entrepreneurs showcasing resilience in high-stakes sectors. US corporations, like the New York Power Authority, shared insights on collaborating with Israeli energy tech companies, emphasizing the importance of global partnerships in addressing climate challenges.

Partners

Trusted partners pave the path to lasting impact

Investor Snapshot

Check out the

local investment ecosystem

Explore the latest comprehensive review of Israel’s tech ecosystem, with statistical analysis and qualitative insights.

Explore Opportunities

Engage with Israel’s largest community of innovators and discover your next business opportunity.

Harness the power of Israeli innovation with

Startup Nation Central by your side.

Startup Nation Central by your side.